The Bank of England’s Monetary Policy Committee (MPC) was split 4/4 over whether to raise the Base Rate at their latest meeting, so it was down to the Governor’s casting vote to hold at 5.25%.

Inflation figures for September have just been released and don’t add much to our knowledge. CPI at 6.7% is slightly below the Bank’s latest forecast, the October figure should show a marked improvement as energy base effects drop out of the comparison. At present, the expectation is that the MPC will hold again in November.

The US Federal Reserve also held their rates (at 5.5%) but longer-term rates jumped, the ten-year to 4.8% and thirty-year close to 5%, doing the monetary tightening job for them. The sheer scale of funding required by the US is weighing on markets, not to mention the lack of any leadership in the House and the inability of Congress to function in the face of a Middle East war and looming US Government shutdown (again…)

Since the optimism of late January/early February, UK interest rates have been on a steep climb. The Base Rate is 1.75% higher as is the 2-year Gilt yield, while the 10-year and 30-year Gilt yield have both increased by around 1.5%. Of course, this implies equally sharp falls in the capital value of bonds. The effect of duration* means that this has been felt much more at the long-dated end of the market: the 30-year Gilt has fallen 21% since early February, the 10-year by 11% while the 2-year is down by just 3.5%. As we have been saying all year, avoid the long end and keep duration low.

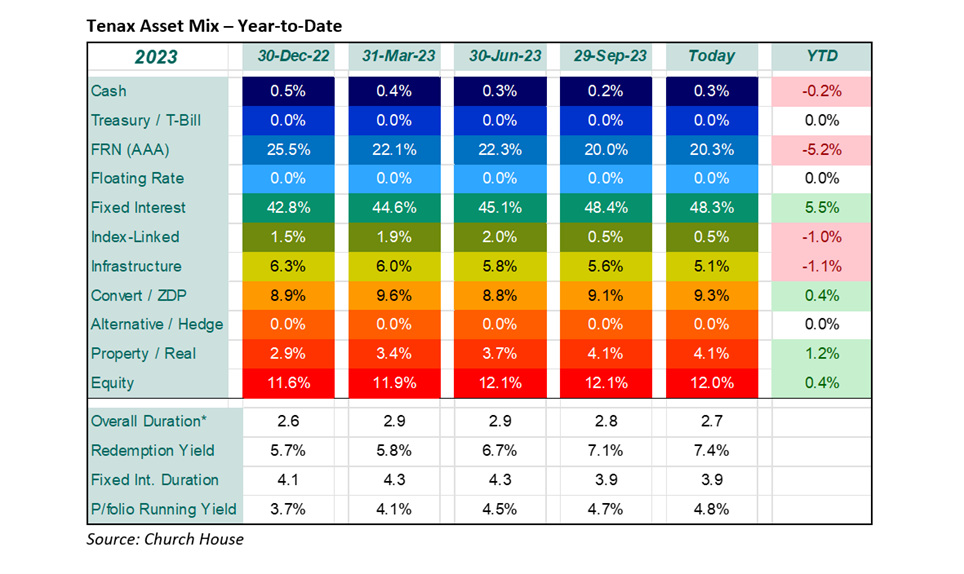

Within the Fund’s portfolio we have again been able to increase the redemption yield at a decreasing duration*. This is a combination that would have been the stuff of dreams a year ago and beyond the realms of imagination for the previous ten years.

*Duration represents the number of ‘periods’ that it will take to repay an initial investment in a fixed interest security. It is not the same as the life of the bond or time to maturity, which will be longer. It can also be viewed as a measure of the sensitivity of the price of a bond to a change in interest rates.

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?