The shortest, darkest day of the year feels quite appropriate as 2022 draws to a close.

An unpleasant year for investors as a savage re-pricing of debt followed the belated realisation by (most) central banks that they had missed what was happening to inflation. Inflation that was being fuelled by their lax monetary policies, supply problems in the wake of the pandemic, and by the ghastly Putin’s savagery in Ukraine.

Over the past couple of weeks markets have been rattled again by ‘tough talk’ from central bankers in the wake of their latest (expected) round of base rate increases. Hardest to take, and definitely the most galling, was the commentary from the European Central Bank:

“We decided to raise interest rates today, and expect to raise them significantly further, because inflation remains far too high and is projected to stay above our target for too long”.

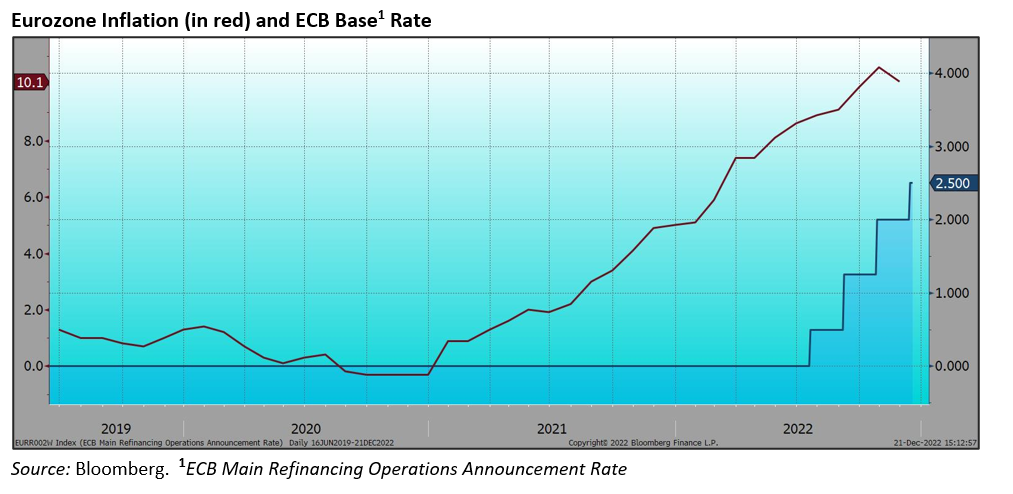

That’s rich coming from the Bank that waited so long to take any action at all (see chart, right) despite what was happening and multiple warnings from observers*. Inflation began to move away from the ECB’s target zone in summer 2021, but it was not until more than a year later, in July 2022 that they even managed to lift their rate off the floor, all the while carrying on with quantitative easing (pumping more money into the system, now wonder it fell in value...)

As mentioned, the Federal Reserve, ECB and Bank of England all raised their base interest rates by 50bp this month, earlier expectations had been for more 75bp increases. But another pleasant surprise from the US inflation figures for November, marking the fifth monthly decrease, tempered the Fed’s response. The Bank of England’s 50bp increase was accompanied by the rather discouraging note that two members of the Monetary Policy Committee had voted to leave rates unchanged at 3% and one had voted for an increase to 3.75% (it is a nine-person committee). It would appear that we are getting close to the peak in these rates, though further encouragement from the inflation figures on this side of the Atlantic would be helpful.

In the past couple of days, the Bank of Japan has thrown in more confusion with a surprise lifting of the cap on ten-year Japanese bond yields (there is even some inflation in Japan). But with the central bank owning something close to 50% of Japan’s (huge) national debt, comparisons with the West can be misleading. It probably does mark the end of the fall in the value of the yen, which has now recovered 12% from mid-October lows.

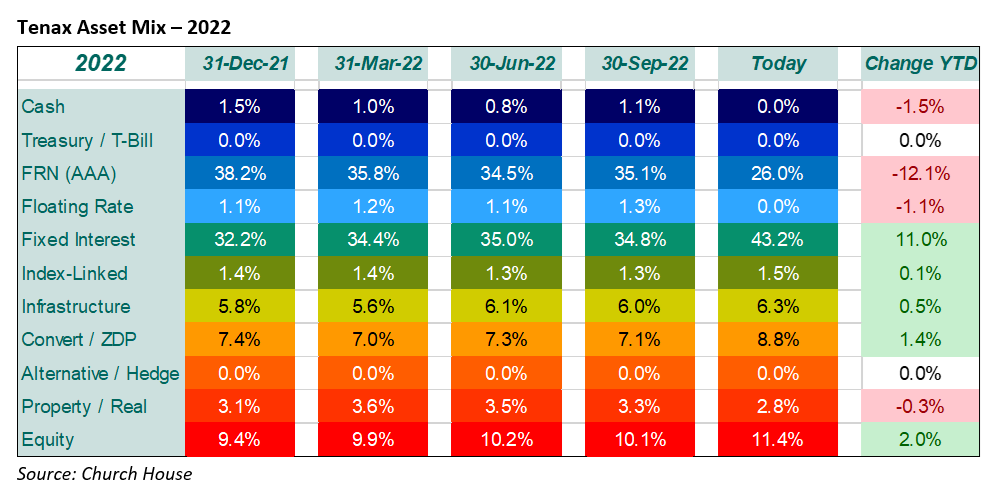

Within the Fund we have accelerated the switch from floating to fixed rate investments, the feature of the final quarter of the year, as fixed interest has become increasingly attractive, particularly at the short end:

This is best illustrated by example. The primary market in fixed interest has recovered (as have credit spreads) but new issuers are offering attractive terms. The Deutsche Pfandbriefbank came to market with a new issue of senior preferred debt maturing in December 2025 with a coupon of 7.625% (incidentally it is also a ‘green’ issue). The NatWest Group brought a new issue maturing in June 2033 (but it has a call in March 2028 which we expect them to exercise) with a coupon of 7.416%. So, while the yield on our floating rate notes is now approaching 4%, the opportunity to ‘fix’ these high coupon returns is very attractive for the Fund.

Elsewhere, the Property / Real exposure is lower as we took profits from our holding in Freeport-McMoRan, which we had established in September, principally as exposure to copper, and this had done well for us. The pure property holdings have had a dull month, but some are looking overly depressed; we have established a new holding in the warehousing and logistics specialist Segro and added further to the new holding in Primary Health Properties. In Equity we have taken a small step into the US technology arena with an initial purchase of Amazon.com, which is now back at 2018 levels and looking distinctly un-loved.

Best wishes for a Happy Christmas and somewhat better markets in 2023

*In January 2022, we wrote: “Inflation is the real bugbear for the moment and a particularly difficult one to tackle. It is not just a UK problem, writing this, US inflation for December has just been reported at an annual rate of 7%. The bounce-back in world economies last year led to an equally rapid rise in energy prices and this is now being made worse by supply constraints.” … “Earlier central bank action to reduce/remove their colossal money support and increase interest rates may have had limited impact on the inflation that we are seeing at the moment. But it would certainly have sent a clear message and I remain mystified as to why they consider that economies that are growing so strongly need to remain on central bank life support. It is definitely time to move back to ‘normal’ levels of interest rates and stop pumping money into the system. If they can’t do this now, when can they?”

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?