The first quarter of 2025 is proving to be an exciting one. Volatility has been the beneficiary, along with the price of gold.

With so many investors sucked in to the dominant US stock markets at the end of 2024, particularly the technology stocks, a change in direction was never going to be comfortable. Here and there it has been savage, even the thick-skinned Elon Musk cannot be enjoying the 40%+ fall in the Tesla share price.

The bond markets have been fascinating. While the US dollar and stocks have been falling rapidly, the same is not true of US bonds, which have been rising. The US ten-year Treasury yield hit a peak in mid-January but has been falling consistently since then, it is now down to 4.3%, with mounting concerns that the policies being pursued by the new Trump administration will lead to a slowdown. Even President Trump has talked about a ‘transition period’ while ducking questions about a possible recession.

The US Federal Reserve is decidedly on hold after their quarter point cut to 4.5% in December. They will certainly wish to see quite what the impact on inflation might be of all the tariffs, possibly counter-balanced by the activities of the DOGE. The ‘Fed put’ is probably still there if the US economy does turn down sharply from its current lukewarm state, but they are not going to be in a rush to help.

The Bank of England is in a bit of a bind, the MPC did cut a quarter point off the Base Rate in February, taking it down to match the Americans at 4.5%, but further cuts are unlikely for a while now as inflation edges back up (some economists are suggesting that it may be back over 4% in the second half). With the economy still moribund, at a time when we must increase defence expenditure, it is hard not to conclude that the Government will have to increase its borrowing again. So, the long end of the Gilt market has been having a difficult time of it and the thirty-year Gilt yield is up at 5.3%.

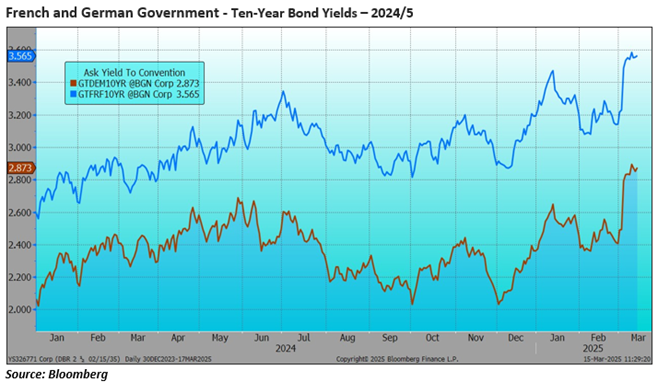

Early this month, the European Central Bank cut rates again (to 2.65%) but this too looks like the last we will see for a while. Of course, the real story here is the decisive (comparatively speaking) result in the German Election and the pace at which Friedrich Merz is moving to release defence expenditure from the constraints of the German ‘debt brake’. European bond markets moved quickly to ‘price in’ extra supply, bond prices sank and yields jumped to their highest levels for a while, right.

December’s volatility in US stocks was followed by an equally volatile January before the reality of the new Trump Presidency really began to sink in and the markets cracked. It would appear that all that talk of US ‘exceptionalism’ marked a turning point. This shows the one-year performance of the NASDAQ Composite Index, which has borne the brunt of the set-back, the yellow line is the 200-day moving average, right.

As with December, European markets have moved in the opposite direction, led by German stocks, and accompanied by a scrabbling sound as managers attempted to unwind their overweight America underweight Europe stance. The aggressively rude behaviour of J D Vance in Europe, the shocking treatment of President Zelensky in Washington and the on/off pile-up of tariffs have completely changed the mood. 25% tariffs against Canada (Canada!), what a ludicrous way to behave.

I suspect that US markets are actually rather more worried by the effects of the slashing of the Federal Government workforce rather than tariffs, the US has such a powerful domestic economy that tariff changes at this stage can be viewed as more of a problem for the rest of the world (though, of course, this will come back to bite them later). But large swathes of the US economy rely on business with the federal government and these cuts bring massive uncertainty and then there is the whole question of who are the people losing their jobs, many veterans move from the armed forces to jobs in federal administration… Americans are going to need to see some enticing tax cuts soon (not altogether easy at the moment) and the promised deregulation, or the mood will sour quite rapidly for the new administration.

So, believe the switch out of (expensive) US stocks into cheaper European stocks and even cheaper UK stocks. UK Gilts appear to be back to the attractive end of the range now but still stay short duration, there is just no advantage to be gained from adding the volatility of longer duration stocks.

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?