Markets marched higher through the summer months, with US equities powering through previous all-time highs.

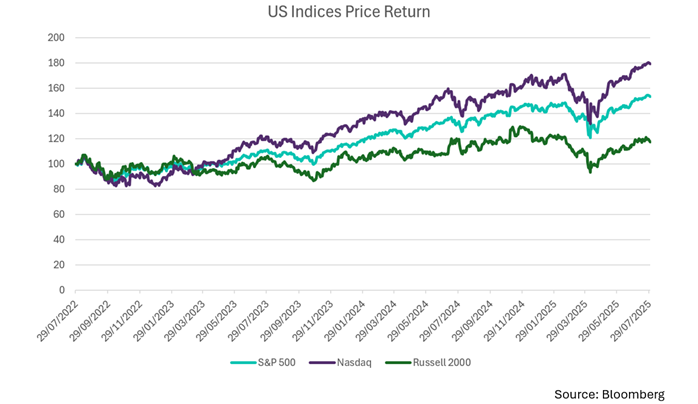

This rally has been driven by a relatively small number of mega cap stocks (the Magnificent Seven being the epitome of this), while mid and small caps have been left behind. We have all seen the AIM market struggles in the UK, but the Russell 2000 index of smaller companies in the US has also lagged, delivering a return of 17.3% over the last three years compared to 53.5% for the S&P 500 and the Nasdaq at 79.3%. The likes of Nvidia and Microsoft are clearly wonderful businesses, but equity markets look vulnerable if these behemoths were to miss a step.

Our top performers within Esk during July (and indeed this year) have been in the Technology and Financials sectors. Standard Chartered could be in danger of reaching highs made back in 2010 if shares continue at this rate. It may have taken 15 years, but management look to have done an excellent job diversifying the bank away from its excess exposure to commodities and instead managed to leverage their relatively unique position as a global mid-scale banking provider, backed by a UK-listing. Euronext, the French-listed stock exchange are also enjoying an excellent year as they are direct beneficiaries of heightened market volatility.

In the world of US Tech, extraordinary numbers seem to be the norm. There are now ten listed companies bosting a market value over a trillion dollars (care to list them all?), one of which (Microsoft) regained its crown as the largest position in Esk during July thanks to remarkable quarterly growth from their Azure division reported last week. Oracle shares had been somewhat unloved in the Tech sector up until 2025, but they have made up for lost ground with shares doubling from their April lows. Oracle Cloud Infrastructure (OCI) has grown rapidly this year, while AI partnerships with the likes of OpenAI and Softbank have generated much excitement.

It has been a volatile first few months as shareholders in Novo Nordisk and their most recent results bought the disappointing news that their Wegovy and Ozempic drugs have grown slower than hoped in the US due to a combination of Eli Lilly’s rival drugs having greater success and ‘copycat’ compounded drugs continuing to hold significant market share despite no longer having FDA clearance. Novo shares now trade on their lowest multiple for many years – we are in the process of reviewing the position.

Our luxury names Hermes and Ferrari saw some share price weakness as both businesses pointed to more muted demand in their latest market updates. This does not come as a surprise given what LVMH have been saying for a few quarters now – nonetheless, we see all three businesses as unique assets to hold for the long-term and will be on the lookout for opportunities to add to our positions if shares do drop further.

August has seen a pickup in volatility (and corresponding fall in markets) on a weaker US Jobs Report and Donald Trump’s administration moving the goalposts on global trade (again). One senses that markets might have got somewhat complacent over the summer months and that we are overdue a dose of reality, but perhaps the Fed will cut rates and ride to the rescue (again).

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?