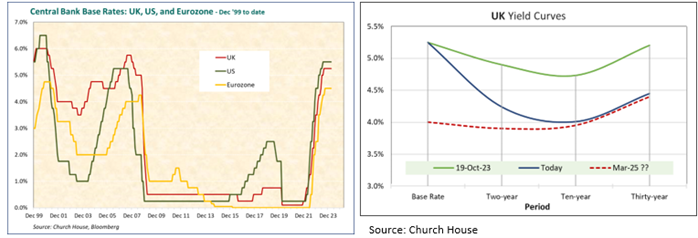

At our recent webinar for the Tenax Fund we showed this longer-term chart of base rates to illustrate quite how steep the recent increases have been, right.

We also observed that the Federal Reserve had done a good job in managing expectations for a speedy reversal. This week, Chairman Jerome Powell has indicated that, while they are still watching the inflation and employment data closely, they do expect to reduce their rates three times this year. Further out they are hinting at a slower pace of reductions. Today the Bank of England has, as expected, maintained the Base Rate at 5.25% but the votes of the Monetary Policy Committee members are now much more in balance with eight voting to hold and one to cut rates.

We expect UK inflation to continue to moderate as we head into the summer and that this will allow the Bank to begin a reduction in rates, probably in June. We remain of the view that the short-dated end of the Gilt and fixed interest market is attractive, while the medium and longer-dated areas have little to offer and could easily turn volatile again. Putting this into graphic form (right), shows the reduction in rates since last October (but not in the Base Rate) along with our suggestion that the curve will flatten out, assuming a more ‘normal’ shape over the year.

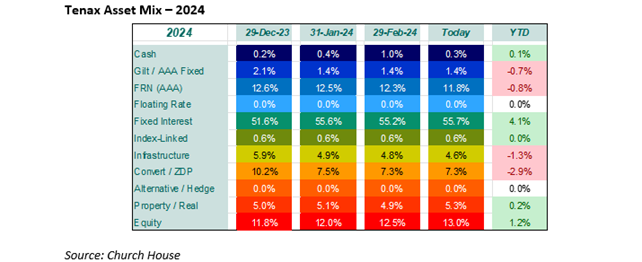

This view is reflected in the Fund’s asset mix. Fixed interest assets are the largest portion of the portfolio but are focused at the short-dated end (see below, current overall duration* is just 3.2), where we can see attractive returns/opportunities. This shows the change over the year to date:

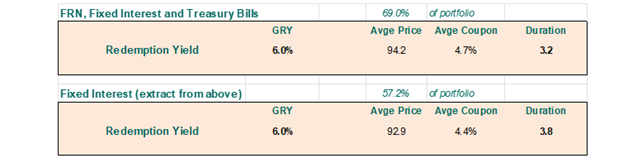

The table, right, shows the overall redemption yield of the fixed and floating rate sections of the Fund’s portfolio, currently 6.0%, a shade lower than last month following the improvement in prices, along with the overall duration. To stress the point that we have made before, the average time to maturity of this book of bonds is 5 years, the duration at just 3.2 reflects the high coupon (interest) stream that the Fund will be receiving in the meantime.

Activity in the portfolio has been low this month. We took an attractive new issue of bonds from the Coventry Building Society paying a coupon of 5.875% and maturing in 2030, which we funded with a small reduction in our NatWest bond exposure, along with some of our floating rate notes from TSB Bank. It has been a positive month for the equity holdings, notably the banks, and for commercial property. Infrastructure remains under a cloud though, maybe, this is showing a few signs of improvement.

*Duration represents the number of ‘periods’ that it will take to repay an initial investment in a fixed interest security. It is not the same as the life of the bond or time to maturity, which will be longer. It can also be viewed as a measure of the sensitivity of the price of a bond to a change in interest rates.

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?